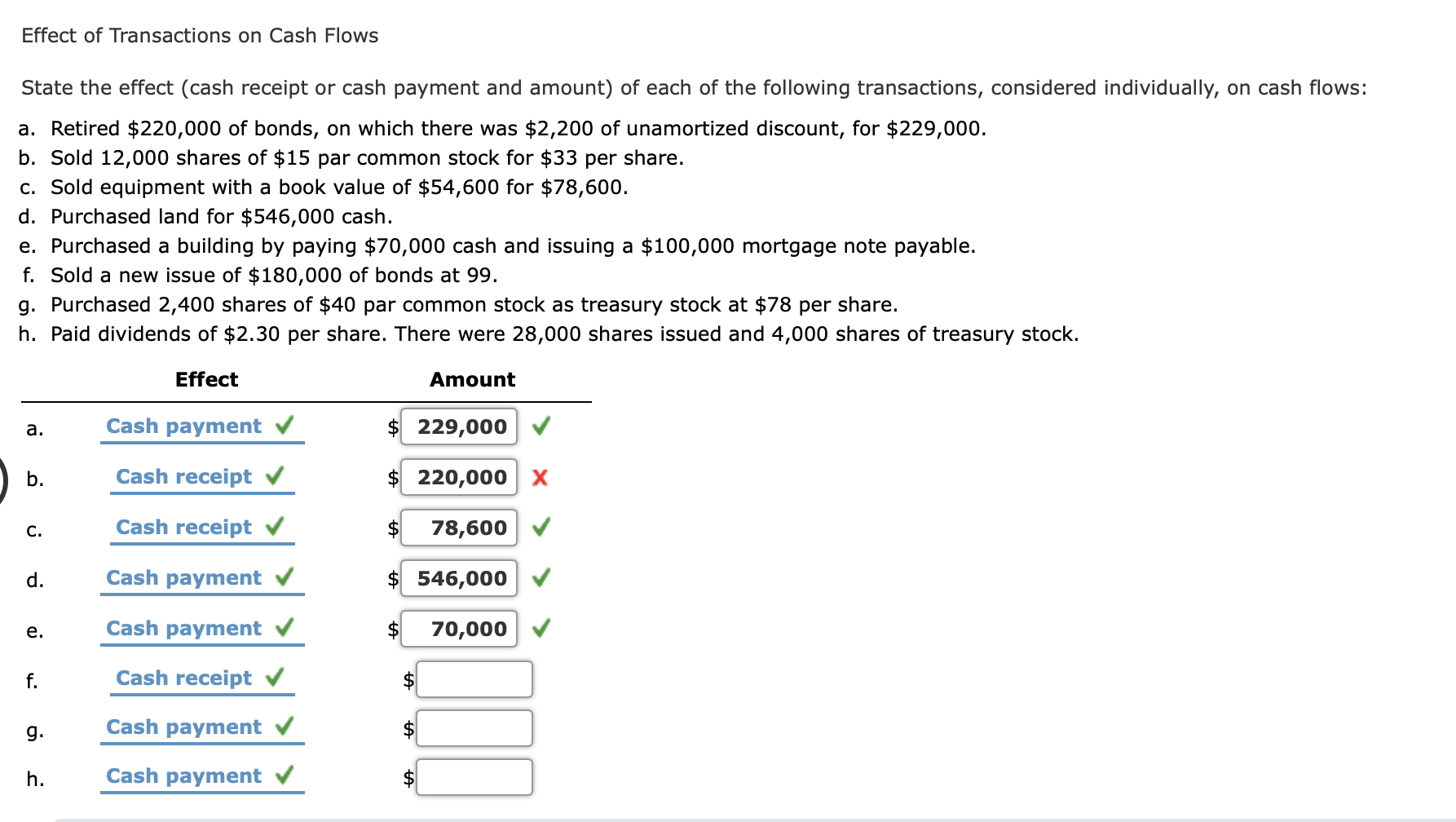

Many corporations also acquire treasury shares as a way of investing in corporate funds. With the exception of the possible impact on the amount of legal capital, these shares are in substance the same as unissued shares and should generally be accounted for under that assumption. Buybacks also represent a defensive strategy for businesses that are targeted for a hostile takeover—that is, one that the management team is trying to avoid. With fewer shareholders, it becomes harder for buyers to acquire the amount of stock necessary to hold a majority ownership position. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Example showing treasury shares journal entry using the cost method

As this partial balance sheet shows, treasury stock is not shown as an asset but as a negative item in stockholders’ equity. The effect of the transaction is to reduce both assets and stockholders’ equity by $24,000. For example, the board of directors may believe that the capital market has undervalued the company’s shares and, accordingly, decide that an investment of funds in treasury stock is worthwhile. The shares of treasury stock are held by the issuing corporation, which cannot exercise any of the rights of ownership apart from the right to sell them. Reducing the number of outstanding shares can serve a variety of important goals, from preventing unwanted corporate takeovers to providing alternate forms of employee compensation. For an active investor, it’s important to understand how the acquisition of treasury stock affects key financial figures and various line items on the balance sheet.

Contents

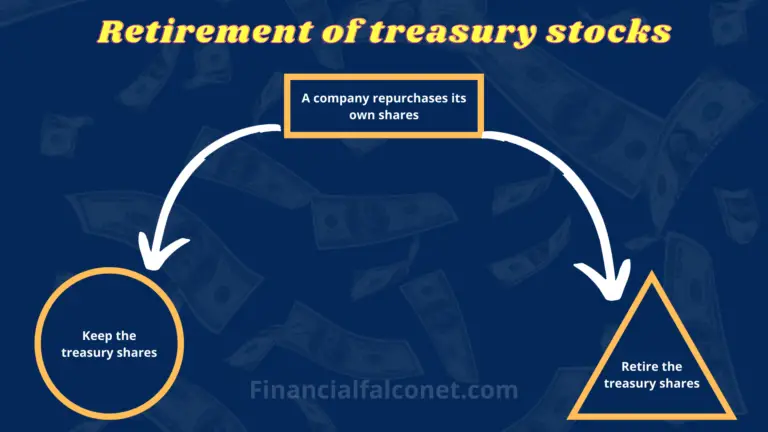

This type of secondary offering happens when a company’s board of directors agrees to increase the share float for the purpose of selling more equity. In order to retire stock, the company must first buy back the shares and then cancel them. Shares cannot be reissued on the market, and are considered to have no financial value. Another reason for acquiring treasury stock exists for corporations whose shares are not traded on an active basis. In these cases, the board may accommodate stockholders by agreeing to buy their shares when they wish to liquidate their holdings.

Accounting for Treasury Stock

The most common methods to buy back their shares include a tender offer or through a direct repurchase. A tender offer involves buying shares back from investors above the market price or at a premium. Companies that do direct repurchases buy shares on the secondary market, just like regular investors do. Assuming the company decides to retire the 100,000 shares, it reduces the total outstanding shares from 1,000,000 to 900,000. As a result, the company adjusts its market capitalization accordingly, totaling $9,000,000.

Example showing the journal entry for treasury shares using the par value method

One reason for this action is to obtain shares for re-issuance when all authorized shares are issued and outstanding. In computing earnings per share (EPS), treasury stock is not considered outstanding and must be deducted when determining the weighted average number of shares outstanding. Since the account is depleted, “Treasury Stock” would still get a credit of $120 million. “Retained Earnings” is debited the remaining $20 million, reflecting the loss of stockholders’ equity. To better understand treasury stock, it’s important to know a few related terms.

For investors, understanding how and why companies use treasury stock can provide deeper insights into a company’s overall financial health and growth strategy. It signals confidence from management and can protect the company against hostile takeovers, giving shareholders a clearer picture of its long-term potential. When a company repurchases its stock, the management signals to the market that the shares are undervalued. This often gives investors confidence that the company is in good financial health and expects future growth, which can positively impact the stock price. Once a company has completed its share buyback, it can retire those shares, hold them for release back into the market at a future date, or provide them to employees as a form of compensation. A buyback comes with both pros and cons, and as an investor it’s important to understand why a company is buying back its shares and how that affects its value for the long-term, allowing you as an investor to make prudent investment choices.

In this journal entry, the company ABC needs to debit the $200,000 into the retained earnings account. This is due to the reacquisition cost of the 100,000 shares is $200,000 more than the amount that the company ABC received when those shares were issued. Retiring treasury stock later after buying back the stock will not affect total equity on the balance sheet. However, the number of outstanding shares on the market will be reduced as a result. In addition to not issuing dividends and not being included in EPS calculations, treasury shares also have no voting rights. The amount of treasury stock repurchased by a company may be limited by its nation’s regulatory body.

It is essential to review each company’s particular laws and regulations to determine the feasibility of resistance. Treasury shares are not counted as part of outstanding shares and don’t contribute to dividends, voting rights, or earnings per share (EPS) calculations. Companies buy back their own shares, turning them into treasury stock, for several strategic reasons. While reducing the number of shares available to investors may seem counterintuitive, this decision often aligns with a company’s broader goals to improve shareholder value and strengthen its financial structure. Treasury stock, on the other hand, represents shares that the company has repurchased from the public. Once reacquired, these shares are no longer outstanding, meaning they don’t come with voting rights or dividend eligibility.

This action goes beyond the acquisition of treasury shares by actually removing them from the issued category. These considerations can help the Company avoid setting a high buyback price for the market. These considerations can help the Company avoid setting a price range that is too unreasonable how to estimate burden and misleading to investors. When shares are retired, they are usually canceled or permanently removed from the market. However, it’s important to note that certain companies may have specific provisions that allow for the issuance of retired shares under certain circumstances.

The organization has to pay for its own stock with an asset (cash), thereby reducing its equity by an equivalent amount. Daniel has 10+ years of experience reporting on investments and personal finance for outlets like AARP Bulletin and Exceptional magazine, in addition to being a column writer for Fatherly. The intuition is that all outstanding options, despite being unvested on the present date, will eventually be in the money, so as a conservative measure, they should all be included in the diluted share count. Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success. He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.

- Stock is repurchased from the money saved in the company’s retained earnings, or else a company can fund its buyback by taking on debt through bond issuance.

- Also known as a follow-on offering or subsequent offering, the secondary offering will occur when a company again places these shares on the market, thus re-diluting existing shares.

- The journal entry for retiring treasury stock may be different from one company to another depending on whether the reacquisition cost of such stock is more or less than the amount the company received when the stock was originally issued.

- A share buyback reduces the number of outstanding shares, which increases both the demand for the shares and the price.

As a shareholder you are not required to sell your shares back to the company in a share buyback; the company cannot make you do so; however, companies do offer a premium over the market price of the share to entice investors to sell. When the number of outstanding shares increases, this causes a dilution of per-share earnings. The resulting influx of cash is helpful in achieving the longer-term goals of a company or it can be used to pay off debt or finance expansion.